How are Trump’s tariffs going to affect New Zealand house prices and residential building? Economist Rodney Dickens takes a look...

![]()

Fallout from Trump’s trade war is only starting. It is possible common sense prevails, and new trade agreements are negotiated between the US and its major trading partners. But a protracted trade war between the US and China seems likely and will have at least a moderate negative impact on global economic growth this year.

Provided the fallout from the trade war doesn’t include a financial crisis that results in banks rationing lending, as occurred following the 2008 Global Financial Crisis, the trade war should be at least a mild positive for the New Zealand housing market, including house prices and residential building.

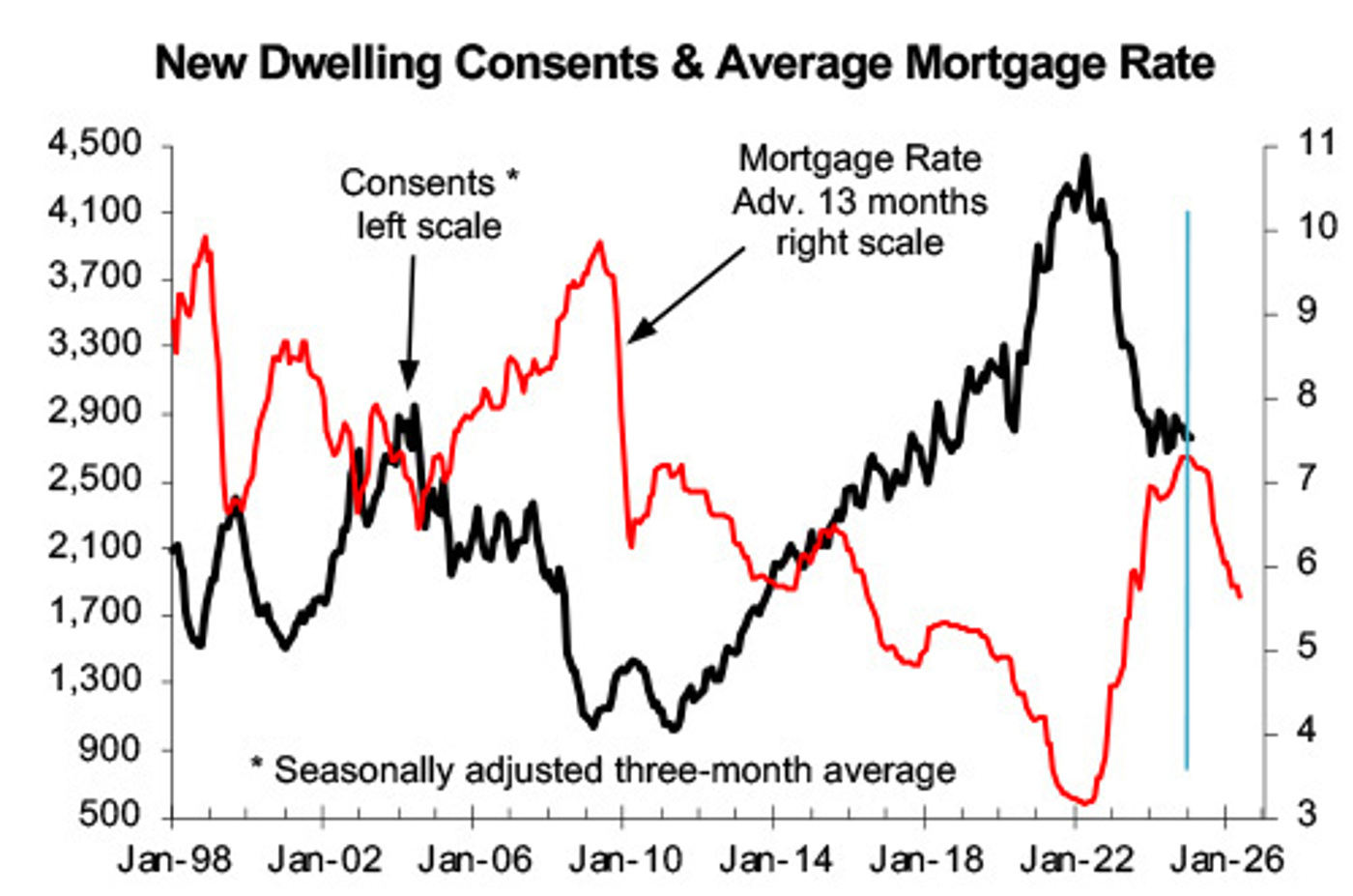

There is already a large stimulus in the pipeline from the fall in mortgage interest rates. The first chart shows the average mortgage rate offered by the major banks advanced or shifted to the right by 13 months as a predictor of national consents for new dwellings.

The Reserve Bank plans to cut the Official Cash Rate (OCR) a bit more, that should result in a further modest fall in mortgage interest rates. And the more economic fallout there is from the trade war the more interest rates should fall this year and extend the upturn in building into 2026.

Covid and its aftermath changed several things, including the relationship between the OCR that is a major driver of mortgage interest rates and global economic growth. However, with Covid long gone as a factor and the partly related inflation problem all but over, the relationship should largely return to what it was prior to Covid.

The second chart compares the OCR with a useful leading indicator of global economic growth I construct from surveys of purchasing managers in the major countries. Prior to Covid, it was common for the Reserve Bank to cut the OCR after falls in the leading indicators that is advanced six months in the chart. This indicator and many like it will start to reflect fallout from the trade war from May. Anecdotes from international shipping companies suggest the leading indicator experienced a sizeable fall from late April.

We live in an increasingly uncertain world, but the more the trade war damages global economic growth, the more the fall in interest rates will be extended. This will extend the upturn in building.

![]()