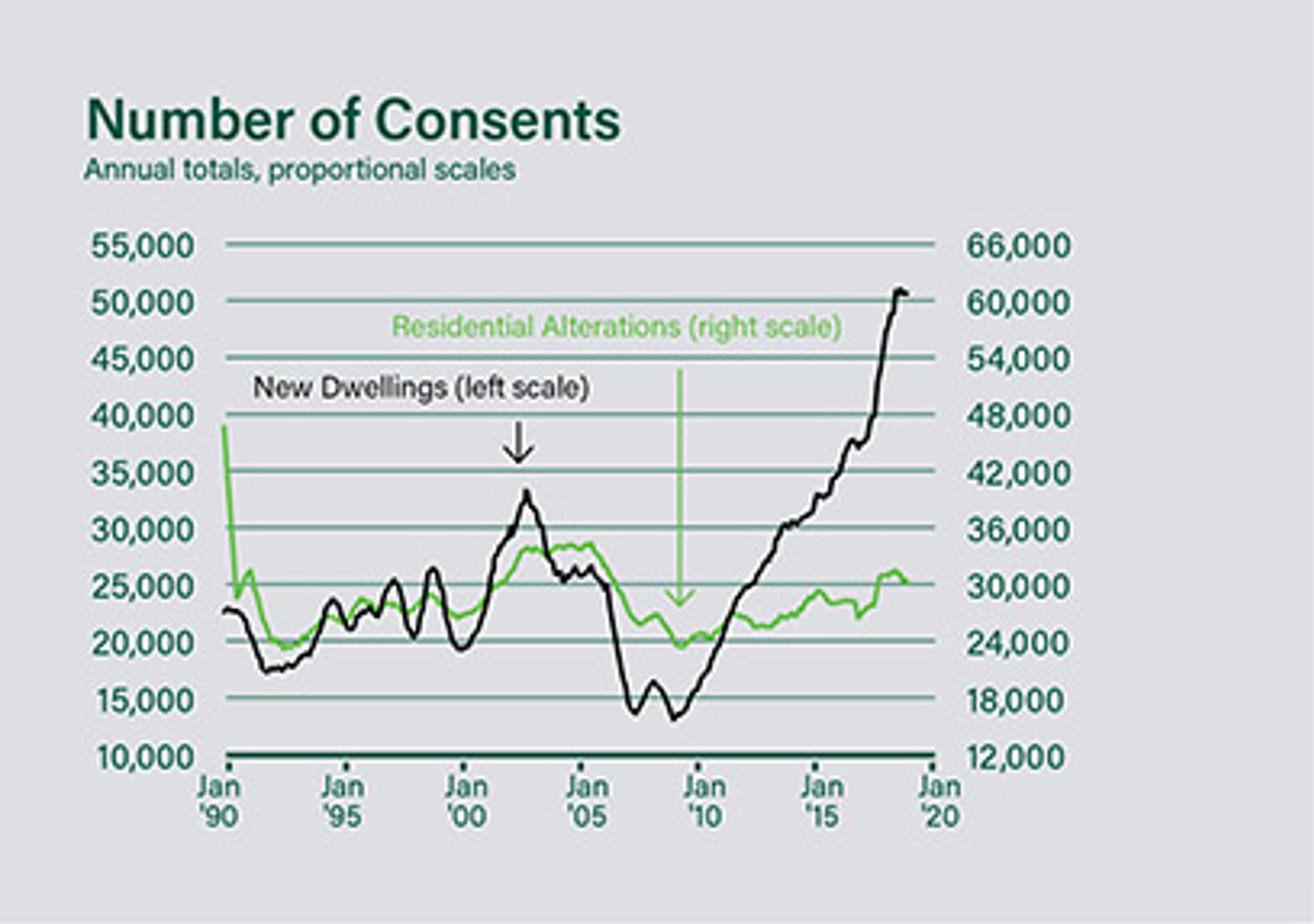

IN THE LAST YEAR AT THE NATIONAL LEVEL, THERE WERE JUST OVER 30,000 CONSENTS ISSUED FOR ALTERATIONS TO RESIDENTIAL BUILDINGS VERSUS ALMOST 51,000 CONSENTS FOR NEW DWELLINGS.

The Reserve Bank continues to charge ahead with OCR hikes without proper consideration of the fallout already in the pipeline, especially for new residential building as discussed in recent articles. This article looks at how much switching to alterations can protect builders against falling demand for new housing.

After the 0.75% OCR hike in November, the Reserve Bank plans to increase it another 1.5% to 5.5% by September 2023. With it taking around 12 months for changes in interest rates to impact on new dwelling consents, this implies consents could keep falling until around the second half of 2024. This is if sanity doesn’t prevail and end OCR hikes earlier.

Over the years some of my building clients have said switching to focus more on alterations has helped them weather major falls in demand for new housing.

In the last year at the national level, there were just over 30,000 consents issued for alterations to residential buildings versus almost 51,000 consents for new dwellings as shown in the chart. This means moderate scope for builders currently focused on new housing to switch to alterations and displace some of the builders currently in that space. However, there are constraints on how much switching can help especially for larger firms.

The national average value per alteration consent in the last year of $83,000 is only 20% of the average value per consent for new dwellings of just over $400,000. The much smaller size of alteration jobs puts a significant limit on how much switching to alteration activity can offset falling demand for new housing.

A second limitation is that during major falls in new housing demand, demand for alterations also falls significantly contrary to what some of my clients have suggested in the past. At the national level, this can be seen in the chart, especially in the major downturns in the early-1990s and 2009. The huge increase in interest rates poses a threat to the level of alteration activity.

Despite these limitations, there is some scope for builders currently focused on new housing to switch to alterations to help insulate themselves from falling new housing demand.

![]()