Existing dwelling sales have benefited from falling mortgage rates, but what does that mean for the demand for new housing?

![]()

Builders in most places should have started to see more enquiries driven by the sizeable fall in interest rates since late-2023. The average mortgage interest rate offered by the major banks was 7.3% in December 2023 and had fallen to 5.4% at the start of July.

Existing dwelling sales reported by REINZ have benefited from falling mortgage rates with an increase of almost 20% over the last 13 months. Existing dwelling sales take around four months to be impacted by interest rates versus around 13 months for new dwelling consents. What happens to existing dwelling sales can be a useful indicator of what is in the pipeline for new dwelling consents.

However, as discussed in the April article, high building over the last few years combined with recent weak population growth has resulted in an overhang of existing property for sale. The overhang has stopped upside in existing dwelling prices despite existing dwelling sales having increased to be close to average levels. The high stock of property for sale will most likely also mean a weaker than normal upturn in new housing demand relative to what would normally be expected given the scale of the fall in interest rates.

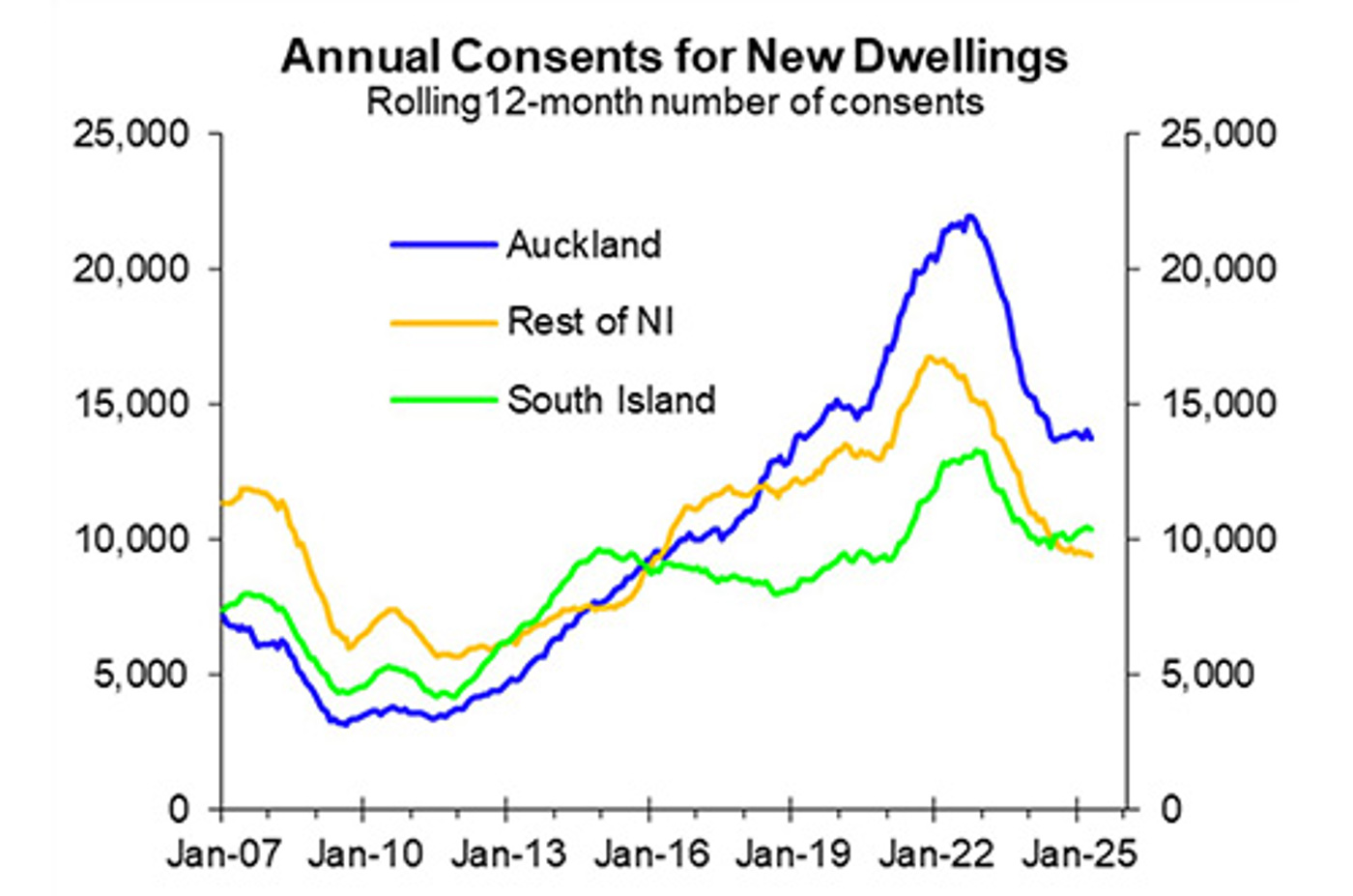

The high level of building was most notable in Auckland relative to many parts of the country. The first chart compares annual new dwelling consents for Auckland versus the rest of the North Island and the South Island. Helped by the Auckland Unitary Plan that made it easier to build higher density housing, it had a dramatically stronger building boom from 2011 to the peak in 2022 than the rest of the North Island and the South Island.

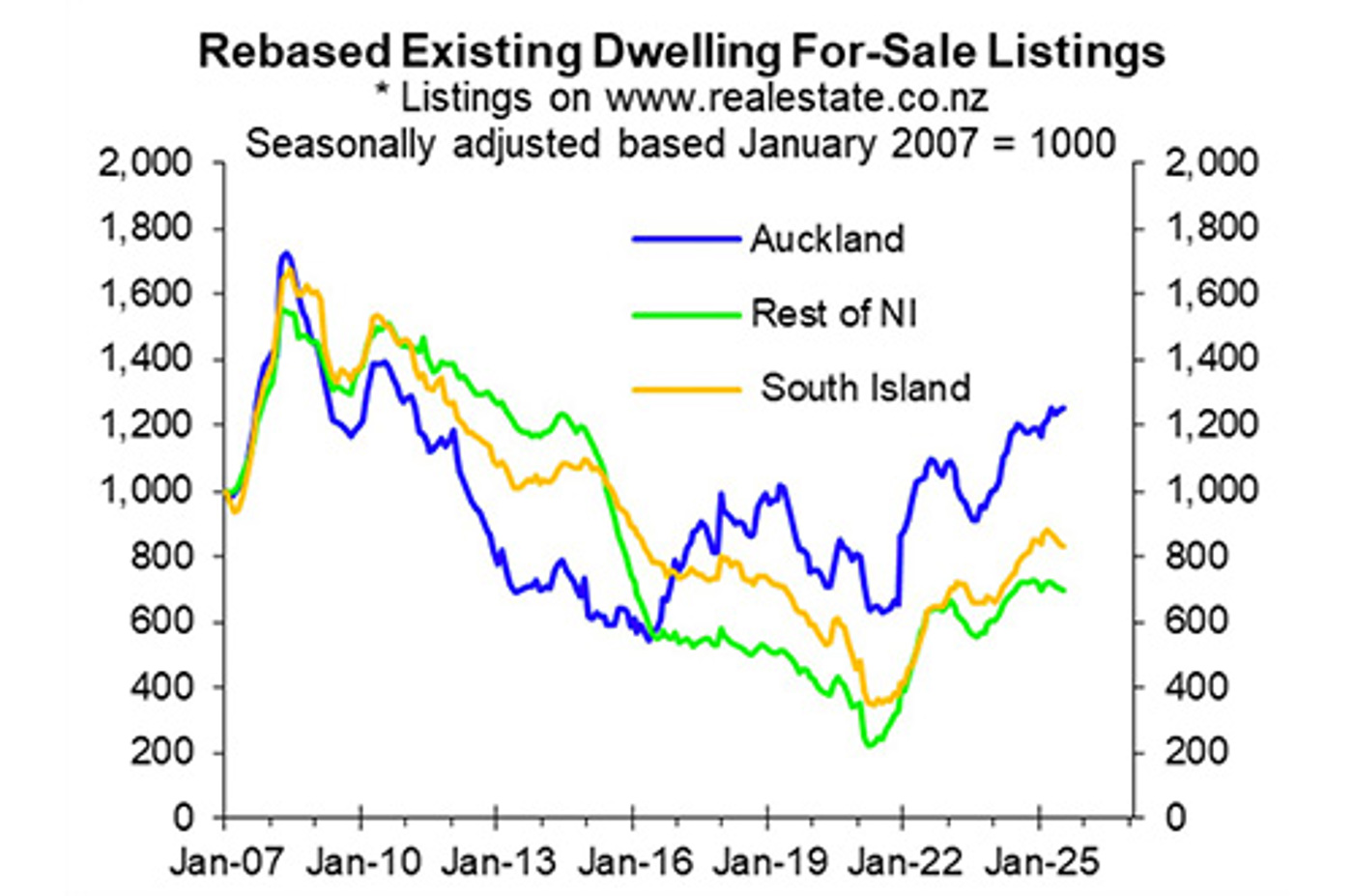

A by-product of Auckland’s stronger building boom is it more than the rest of NZ having a high stock of existing dwellings for sale. The second chart shows for sale listings on www.realestate.co.nz for the three areas with the actual numbers rescaled so they all start at 1,000 in January 2007. This is done so it is possible to see how the three have performed on a relative basis.

Almost all areas of the country will benefit from the fall in interest rates, dampened a bit by still reasonably high stocks of existing housing for sale. The dampening is likely to be more so in Auckland because it is suffering more from an overhang of existing dwellings for sale that includes recently built dwellings relative to other parts of NZ.

To read the referenced article see:

![]()