Despite economic growth having been quite a bit weaker than the Reserve Bank was predicting in the last two quarters – normally a basis for the market to start pushing down interest rates – interest rates have failed to fall. The market has overlooked the weaker than expected economic news, including more than a 20% fall in new dwelling consents, and is instead focusing on the largest inflation problem in over 30 years.

I suggested in past articles there was the potential for at least a temporary fall in interest rates in response to negative news about economic growth and especially residential building. Temporary because the battle against inflation was always likely to be protracted. But it now looks more likely there will not be a temporary fall and high interest rates will continue until inflation is eventually ground down.

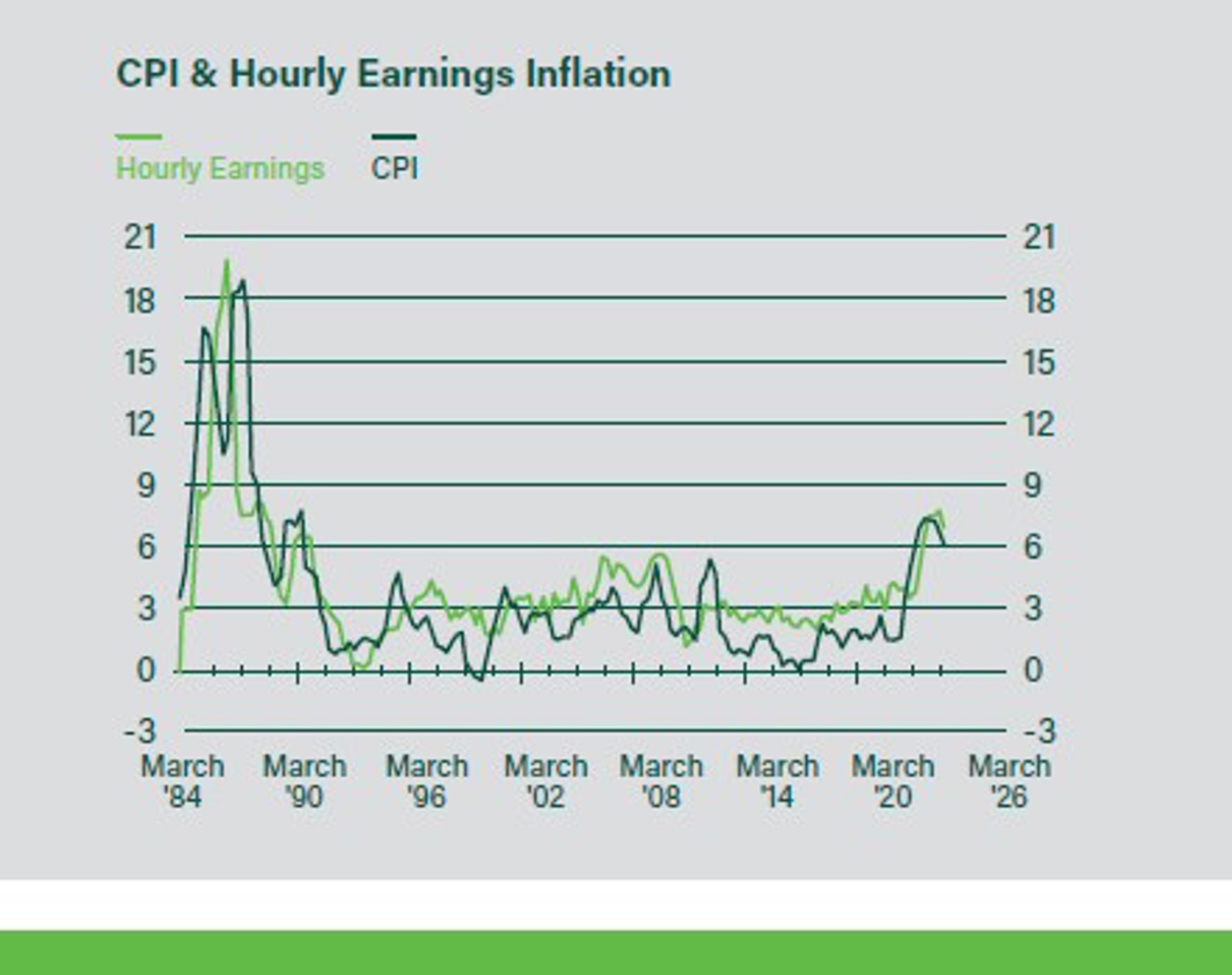

At the heart of the inflation problem the Reserve Bank is battling with high interest rates is a wage-price spiral. Consumer price and wage inflation are at the highest levels since the early 1990s, as shown in the chart. They have eased a little recently, mainly for consumer price inflation because of a lower oil price, but the battle against inflation is likely to be protracted and involve more economic pain.

Based on the historical experiences in NZ, the US, the UK, Australia, and Canada, it takes a major recession or often back-to-back milder recessions to break a wage-price spiral. Those interested can read about this in a recent report I prepared for clients about these experiences (see link below).

It will not be a straight-line process and a temporary fall in interest rates is still possible at some stage. But there will need to be quite a bit more economic pain before there will be scope for a fall in interest rates of the scale needed to drive a solid rebound in residential building. This is best considered in the context of the unemployment rate, at 3.6% most recently, needing to be at 5% or higher to break the wage-price spiral.

For more information see - wage rise spiral report

![]()