Just as improved NZ economic growth will help the building recovery in time by boosting population growth, recent bad economic news has contributed to the fall in interest rates resuming, writes Kiwi economist Rodney Dickens.

![]()

Weak population growth and an overhang of existing property for sale will mean a weaker upturn in residential building than justified by the large fall in interest rates that started in January 2024. With interest rates taking up to a year to impact, many builders should have started to see an increase in enquiries already although this may have been tempered since April by people being a bit cautious because of uncertainty caused by Trump’s trade war.

While a weaker than normal upturn in residential building is likely over the next year, in time population growth should improve. While recent negative economic news, including uncertainty caused by Trump’s trade war, is extending the fall in interest rates that will enhance the building upturn.

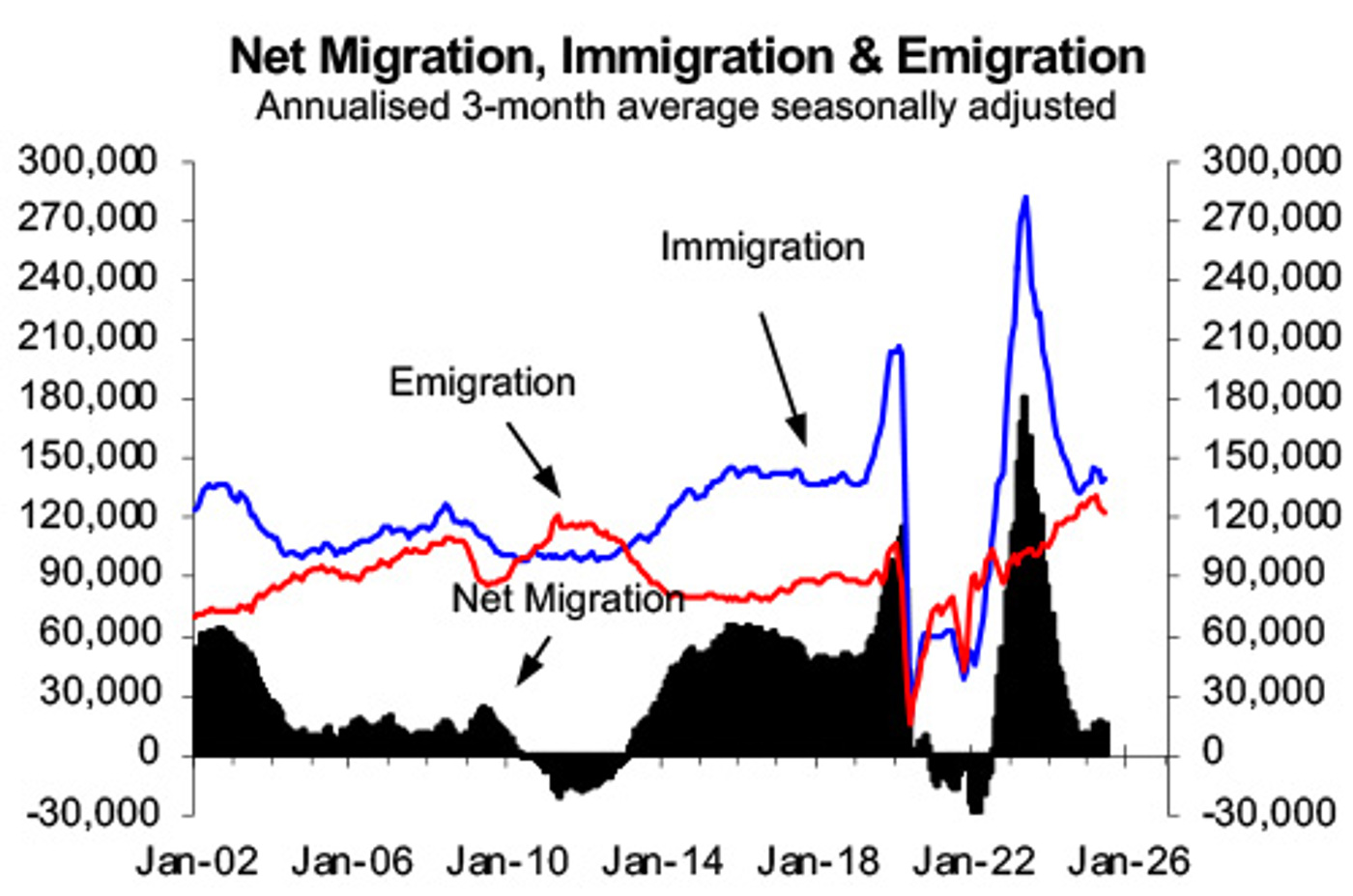

There was a major slowing in population growth in 2024 because the net inflow of migrants – people arriving less people leaving on a permanent or long-term basis – fell sharply, implying less need for extra housing (second chart). But net migration has shown hints of improving and as economic growth and job prospects improve following the 2024 recession – when national economic activity fell 2% - it will encourage less people to leave and more to migrate to NZ including Kiwis returning from OE. As the second chart shows, immigration, emigration and net migration a quite cyclical and job prospects play a major part in driving the cycles.

This includes slightly lower existing dwelling sales reported by REINZ for the last two months, weakness in electronic card spending and falls in most business surveys probably linked to Trump’s trade war albeit for some the fall has been reversed.

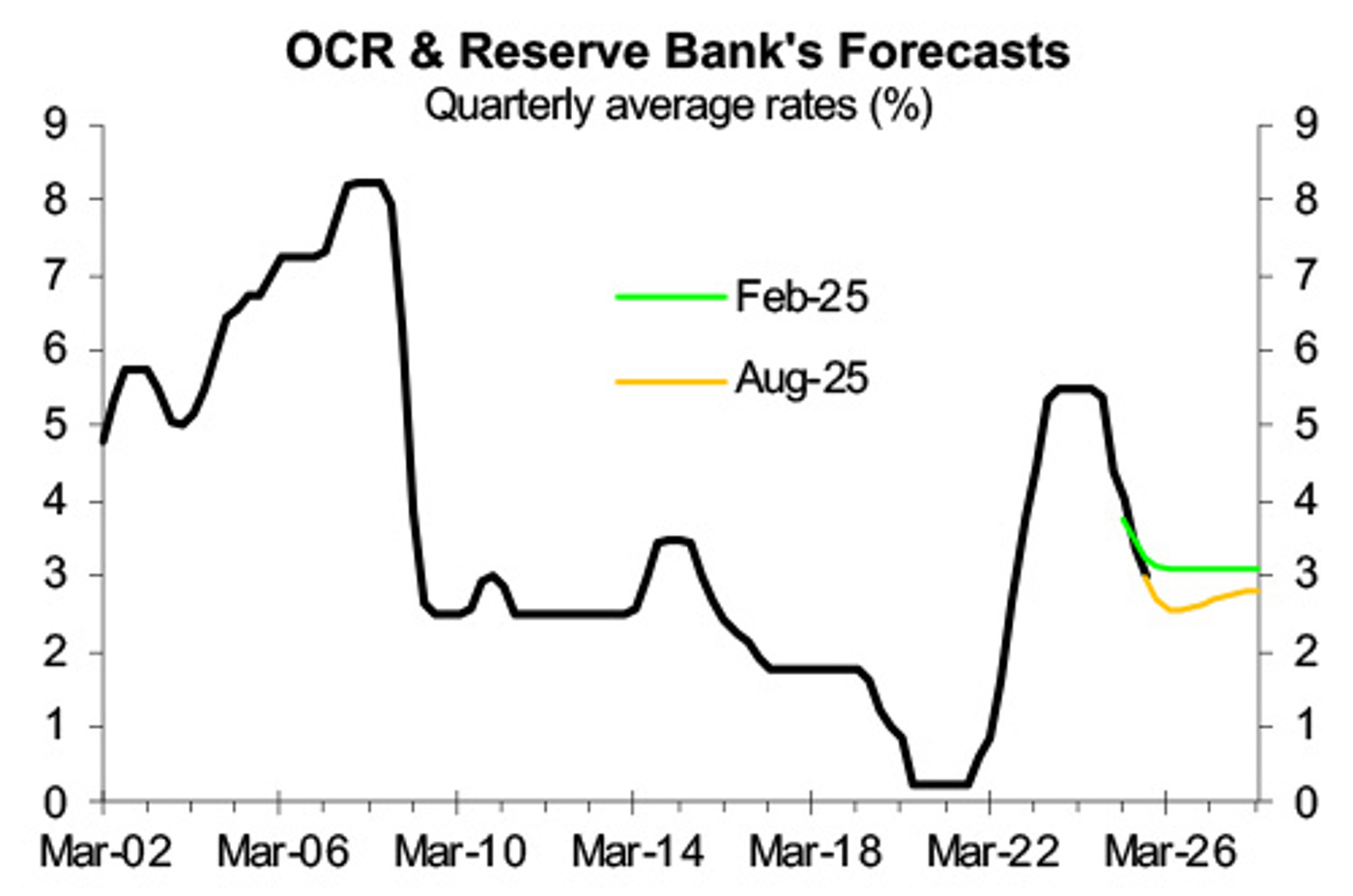

Only six months ago the Reserve Bank was predicting the Official Cash Rate (OCR) that it sets and has a major impact on mortgage interest rates would only get as low as 3% (green line in the first chart). But in August the Reserve Bank cut the OCR to 3% and predicted it would fall to a low of 2.5% by March 2026 (gold line in the first chart). In response, mortgage interest rates have resumed the fall and will fall more especially shorter-term fixed mortgage rates if the Reserve Bank delivers more OCR cuts.

In time the fall in interest rates, improved population growth and potentially abating concern about fallout from the trade war will ensure stronger economic growth. This is likely to fuel some upside in interest rates, but this won’t stop what should be a reasonable upturn in residential building.

![]()