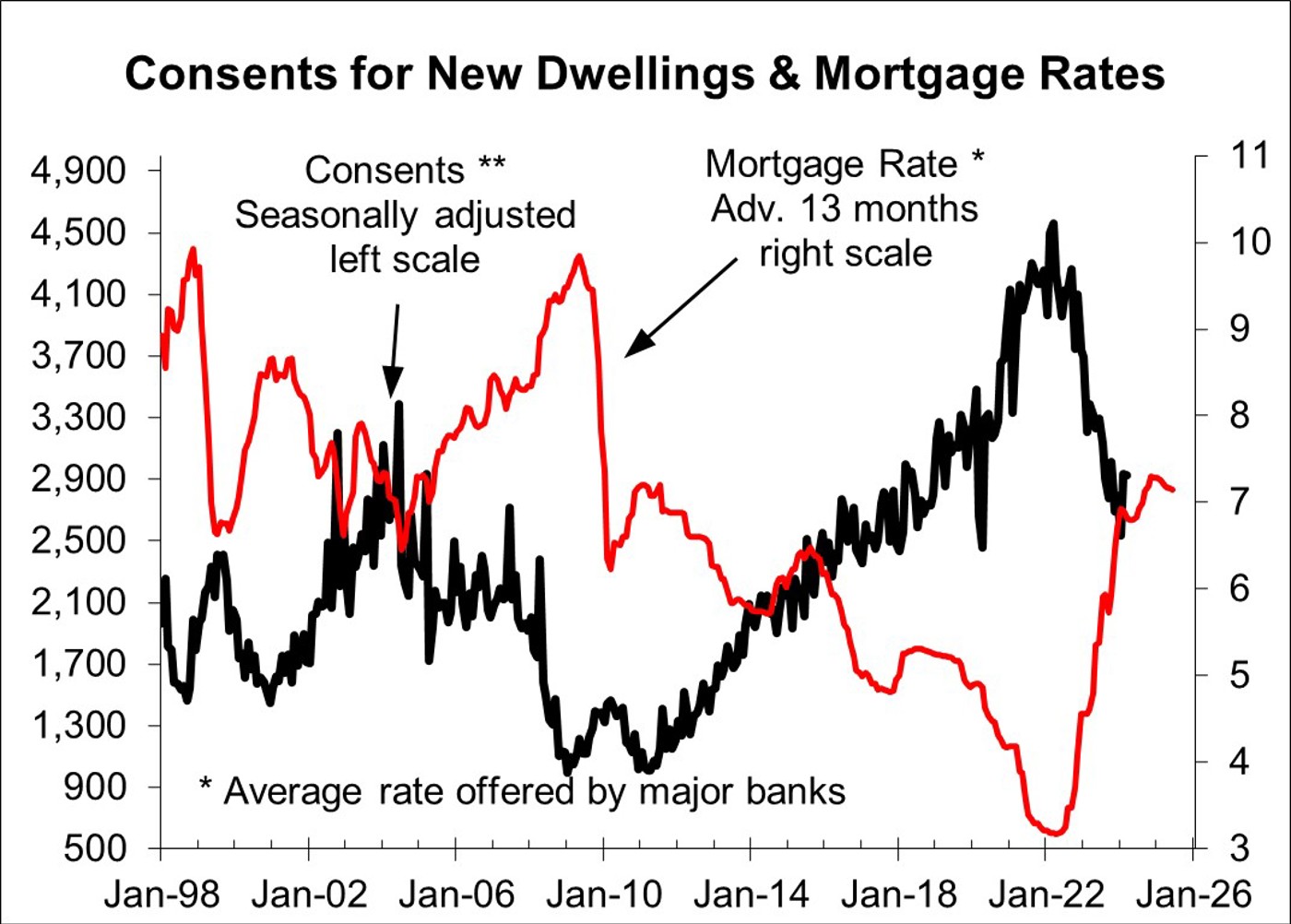

The pain from the sharpest ever rise in interest rates is not quite over, but there are indications some recovery in new dwelling consents will start in H1 2025 and improve thereafter.

As shown in the first chart, below, mortgage interest rates take around 13 months to impact on new dwelling consents. Consents for new dwellings have fallen roughly in line with what the earlier rise in mortgage rates predicted while the tail end of the increase in mortgage rates implies a bit more downside for consents in H2.

There are hints of a fall in mortgage rates that is driven by selective cuts by some banks. Allowing for the 13 months it takes for mortgage rates to impact on consents, a minor rise in consents may start in H1 2025. This implies some builders should start to see more enquiries later this year.

The Reserve Bank doesn’t plan to start cutting the OCR much until H2 2025 with more significant cuts planned for 2026. Allowing for the normal lag, this implies significant upside in new dwelling consents will not occur until H2 2026 and flowing into 2027.

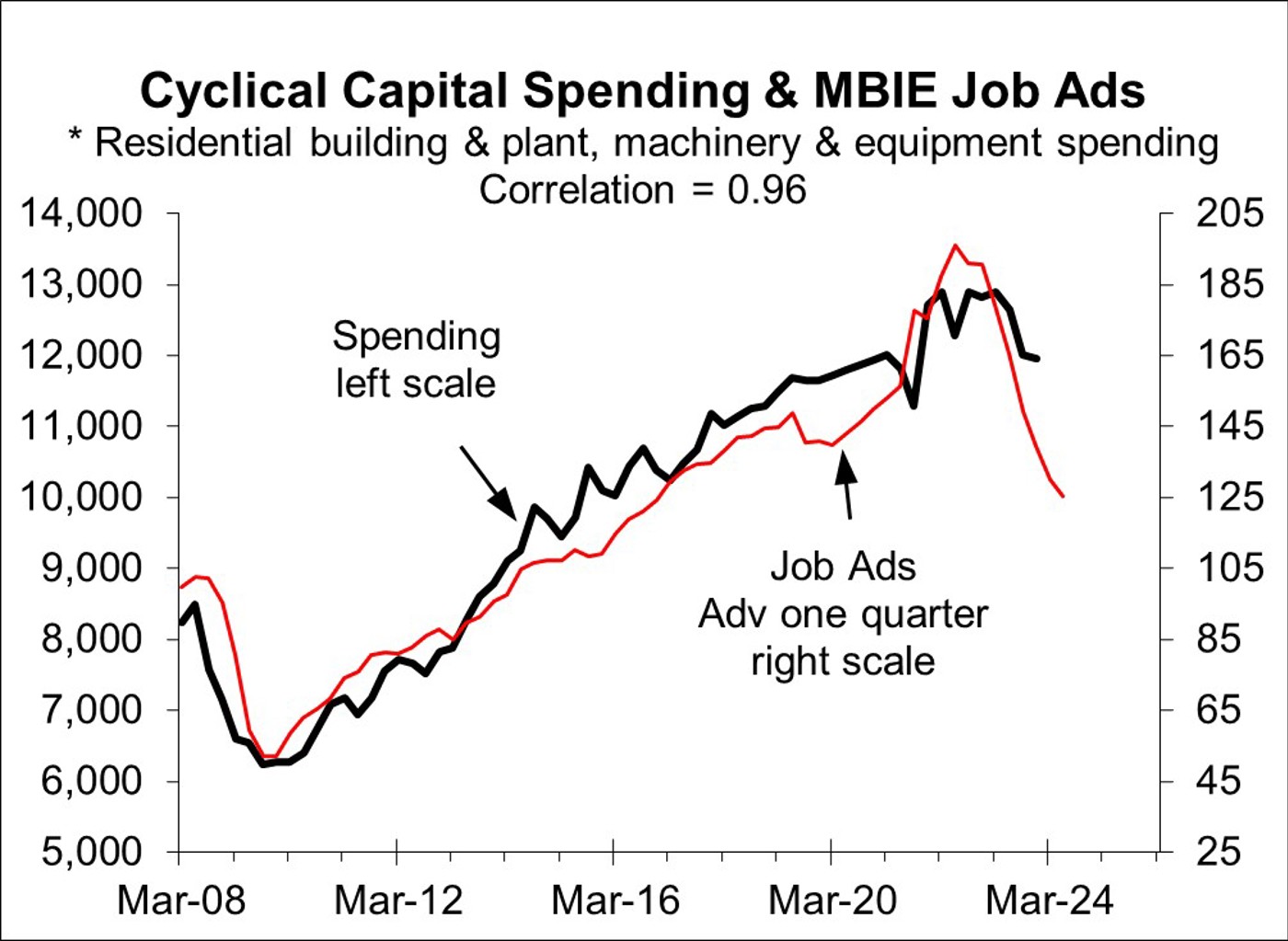

Job ads have already experienced a major fall and can be a useful leading indicator for capital spending that plays a pivotal role in economic upturns and downturns (second chart). The cyclical component of capital spending and job ads have been adjusted to remove the 2020 Covid-driven falls to better show the underlying relationship between them.

The best fit is with job ads leading by one quarter with them updated to Q1 2024 versus Q4 2023 for the cyclical capital spending component of GDP. Allowing for the one quarter lagged impact, the fall in job ads points to significant further downside in cyclical capital spending over H1 2024 and possibly flowing into H2.

It is possible cyclical capital spending will fall 20% from the peak that will take $2.6b or 3.7% off GDP. This is a much worse outlook than the Reserve Bank expects and should mean major progress is made in taming inflation. While the Reserve Bank is likely to be slow to realise the extent of the pain it is inflicting, the market has started to front run OCR cuts by nudging down selected mortgage rates and should get more aggressive in pushing them down this year if I am right about the recession.

![]()