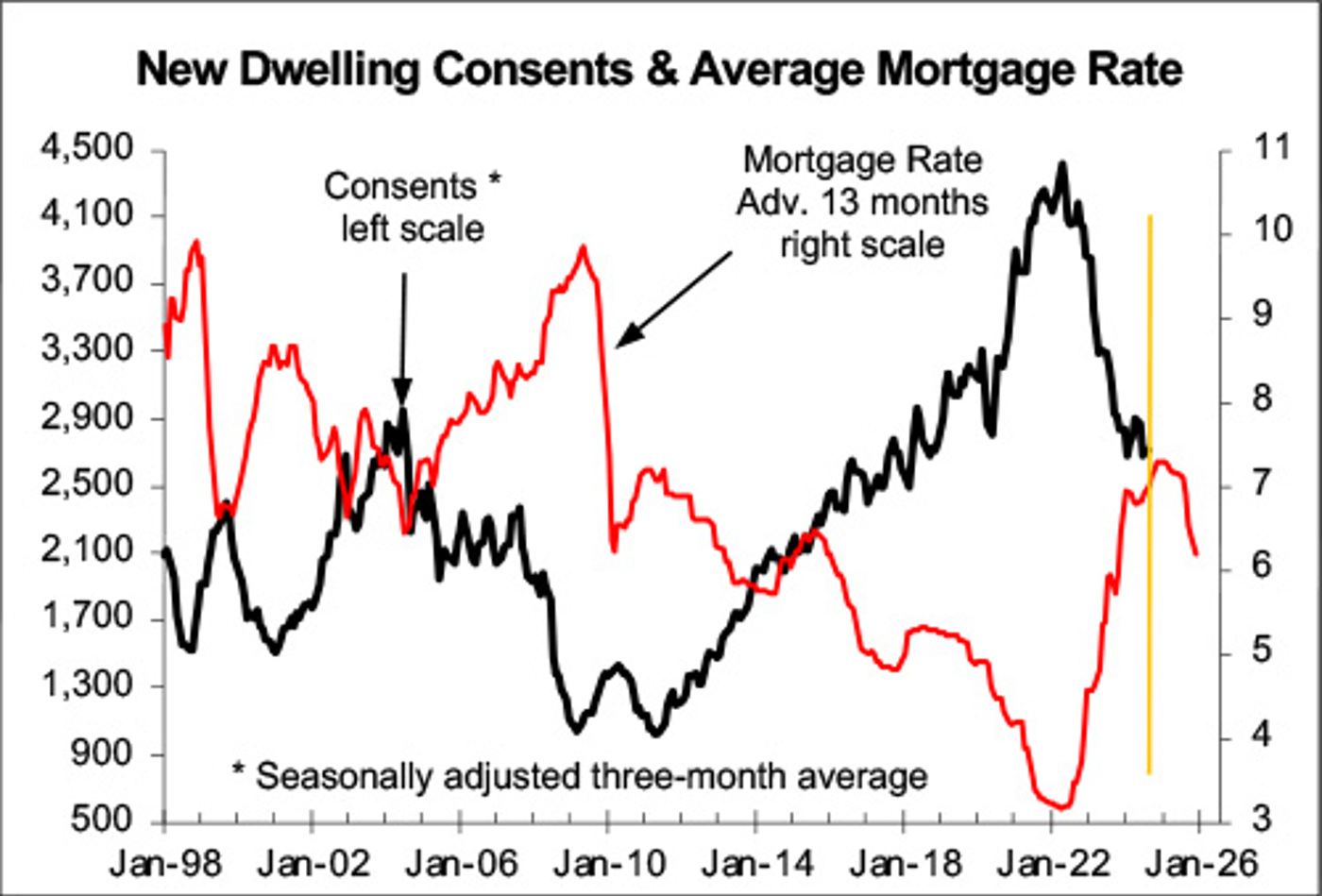

It takes around 13 months for changes in interest rates to impact new dwelling consents, explains Kiwi economist Rodney Dickens.

![]()

There is a boost in the pipeline for residential building from falling interest rates but also negative from much lower population growth because the net inflow of people from overseas has slowed significantly. Traditionally interest rates and net migration have been the most important drivers of upturns and downturns in residential building, but since the late-2018 ban on most foreigners from buying property interest rates have become the overwhelming driver of upturns and downturns.

It takes around 13 months for changes in interest rates to impact on new dwelling consents. This is shown in the first chart, in which consents are on the left scale (black line) and the average mortgage rate offered by the major banks is the right scale (red line). The best fit is with the red mortgage rate line advanced or shifted to the right by 13 months. Falling interest rates over the last year are about to provide a solid boost to consents for new dwellings over the next year given the normal lagged impact.

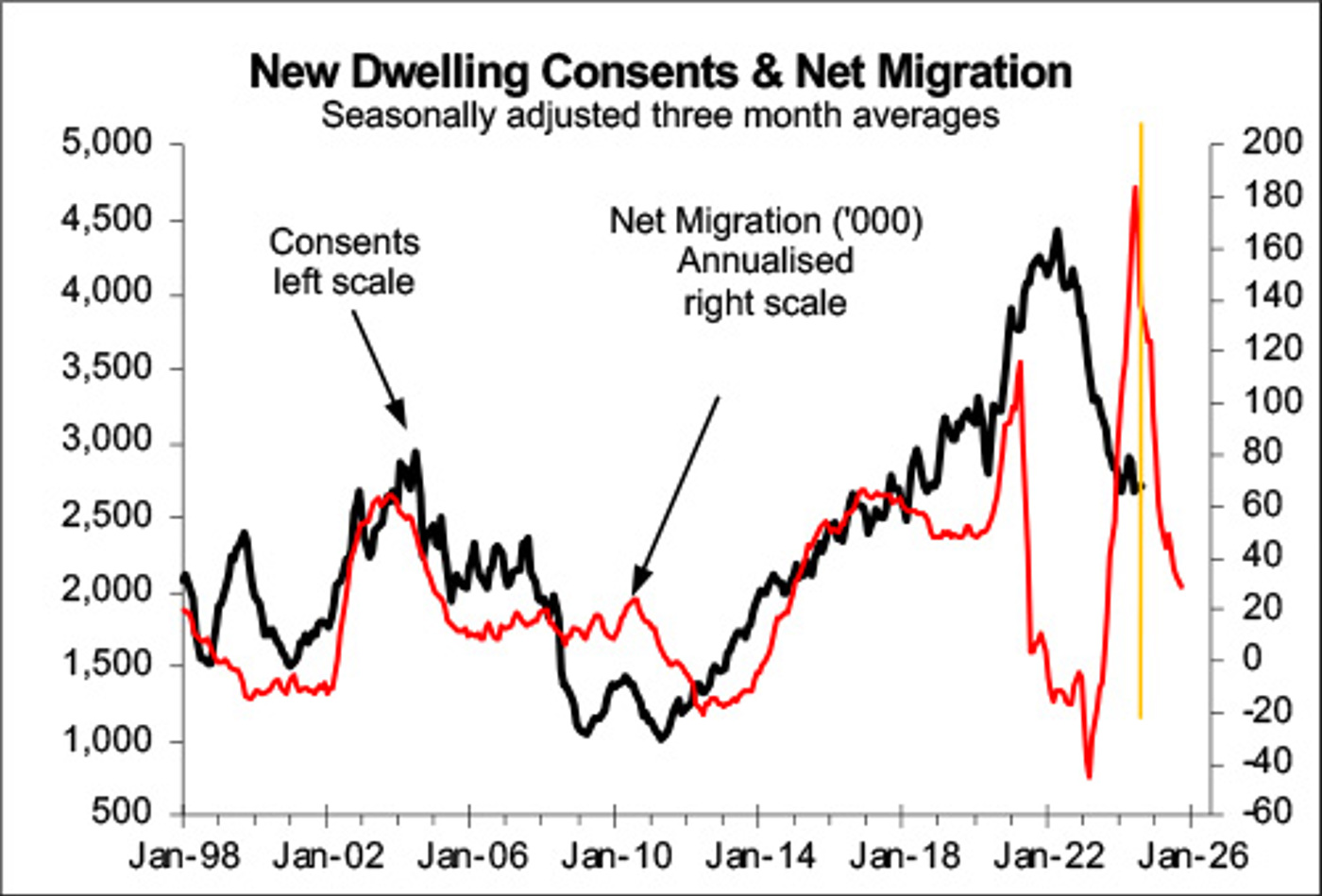

Traditionally cycles in net migration have also played a significant part in driving upturns and downturns in residential building. This is shown in the second chart that has consents as the black line, left scale, and has net migration as the red line, right scale. The best fit is with net migration advanced or shifted to the right by 13 months.

Since the late-2018 ban on most foreigners from buying property, that included immigrants with work, student, and long-term visitor visas, cycles in net migration have had negligible impact on consents.

Since 2018, the behaviour of new dwelling consents is explained almost exclusively by the major cycle in interest rates while the link between consents and net migration has almost completely broken down. The surge in net migration following the opening of the border in 2022 will have provided some boost to consents, but this was swamped by the negative impact of the massive increase in interest rates. The surge in net migration was driven mainly by increased immigrants with work, student, and long-term visitor visas; people not able to buy property other than apartments as presales in approved developments.

The tumble in net migration in the last year has largely been driven by fewer immigrants with work visas. This is why it should have limited impact on consents. This will allow the boost in the pipeline from the sizeable fall in interest rates so far, that should continue the next year, to drive a significant rebound in consents allowing for the 13 months it takes interest rates to impact on consents.

![]()