The worst of the fallout from the sharpest ever increase in interest costs is still to impact the level of residential building here in New Zealand. However, it should have already occurred in general for the level of demand builders are seeing from

new clients.

Nationally, consents for new dwellings have already fallen 27% from the peak level in early 2022. With interest rates taking around 12 months to filter through to consents and, having peaked in December 2022, these should fall quite a bit further over the rest of the year.

Based on my analysis of the drivers of new housing demand, leading indicators like the ANZ survey of residential builders and feedback from a range of building contacts, consents are likely to fall at least 40% from the peak level, possibly 50% or so.

It will not be the same in every part of the country or for every segment of the new housing market, but few areas will avoid a major fall that most will already be dealing with. However, the tendency for a fall in building activity to be followed by upturns should hold true.

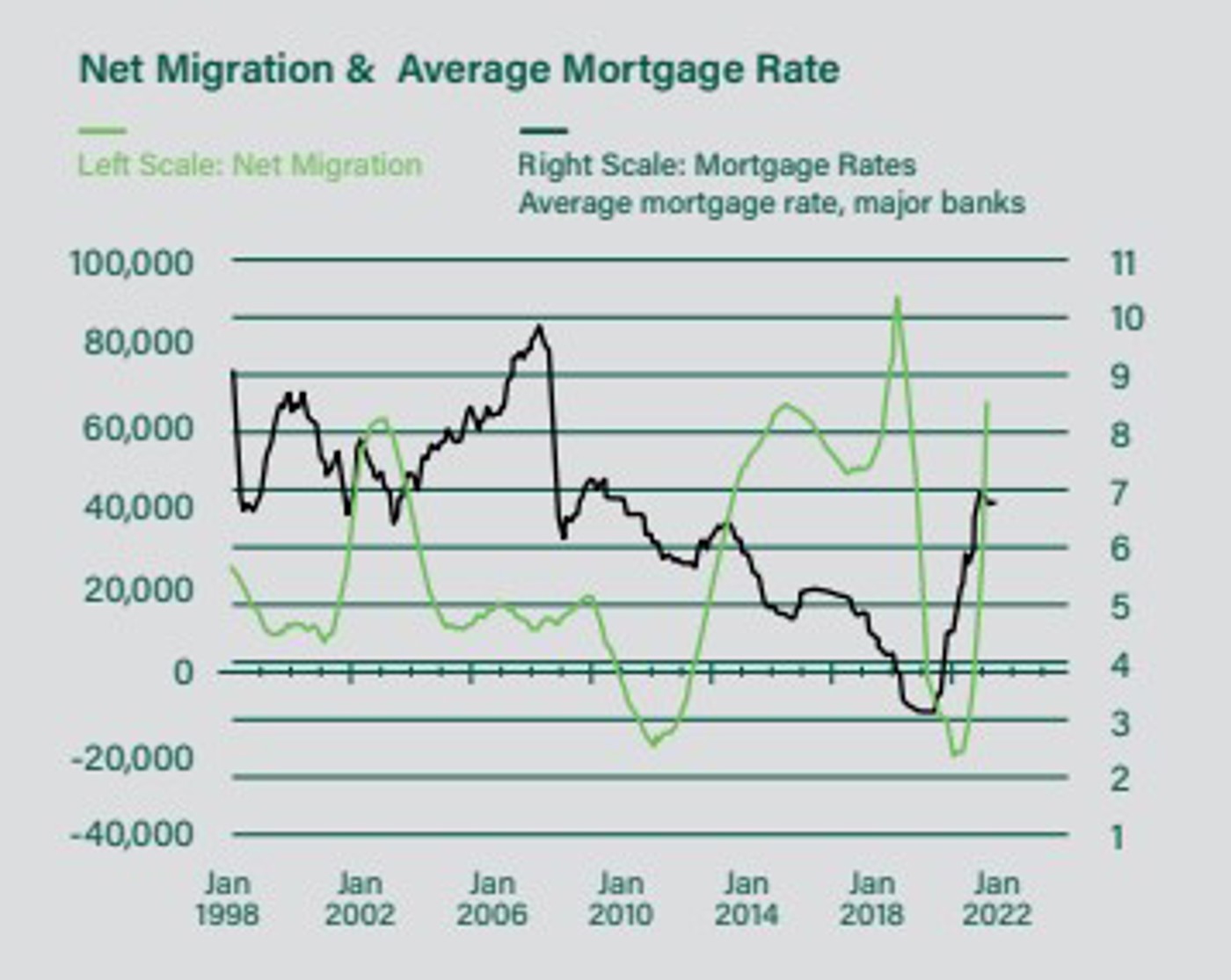

Now the Reserve Bank has signalled the end of OCR hikes, there is the chance for at least a moderate fall in interest rates over the next year as the scale of the fallout from the massive increase becomes more apparent. Critically, the fallout will be quite a bit worse than the Reserve Bank expects, which is key to lower interest rates. For example, the unfolding fall in residential building activity will be around twice what the Reserve Bank is predicting.

Net migration – immigrants less emigrants – is the second most important driver of new housing demand and has rebounded strongly following the opening of the border last year (green line in the chart). Like interest rates, net migration takes around a year, if not a bit longer, to impact on consents but is quicker to impact on demand seen by builders.

From having been super negative, the two main drivers of new housing demand are starting to signal the start of an upturn for next year. How strong and sustained it will be is debatable, but at least there is something positive to consider at a time when things are bleak for many builders.